Bad news, I have to kill you, twice…just momentarily, of course.

Which will cause the most considerable financial distress to your family?

It’s 1, isn’t it, because the little ones are well, little, and rely on you for everything.

In 25 years, they better be hopefully will be financially independent and you’ll be better off too, what with the mortgage almost paid off, savings built up etc.

So why buy a level term life insurance policy that will pay out the same amount now…as it will in 25 years?

Don’t you need more cover now, and less in the future?

Let’s say you’ve worked out that you need cover of €500,000 over 25 years to care of your family should you leave us unexpectedly.

Does it make sense for your family to get the same payout in 25 years as they would today?

Or is there an alternative?

Of course, there is!

A quick crash course on the two types of life insurance available:

a) Level Term Life Insurance

This is your run of the mill life insurance that you’re familiar with. You die during the term, it pays out the agreed lump sum. So if you take out €250,000 over a 25 years term and you die within those 25 years, it pays out €250k to your fam. Simple enough, right?

b) Decreasing Term Life Insurance (commonly known as Mortgage Protection)

This is simply a life insurance policy where the amount of cover reduces over time. If you choose to assign it to a bank for a mortgage, then it becomes mortgage protection. But can buy reducing term life insurance and use it as personal life cover even if you’re not getting a mortgage.

Using our example above but buying €250,000 reducing term life insurance over 25 years:

Reducing ten life insurance creates a new source of money when your family need it most – when the kids are young.

In the future, when they’re financially independent, they don’t need a massive payout.

So buying reducing life insurance instead of level life insurance meets your needs:

It protects your family at the time of their lives when they are most vulnerable

And the real beauty is…

IT COSTS A LOT LESS THAN LIFE INSURANCE

Ally McBeal – now there’s a blast from the past for all you 40-somethings!

Evan thought a €500,000 15 year life insurance policy would be best for his situation.

Hi Nick, I used your price comparison wizard. Given my assets & pension cover etc., I would like to arrange life insurance for €500,000 for 15 years (while we still have kids at home). Both 46, full health etc. It quoted €100 per month. Let me know any other key points to consider. Thanks, Evan

But did Evan need to level life insurance or would reducing life insurance work just as well?

Let’s find out:

Evan was happy to go with the €500,000 reducing cover.

And he used the €41 saved to buy himself an income protection policy which he initially thought was outside his budget!

Pros

Cons

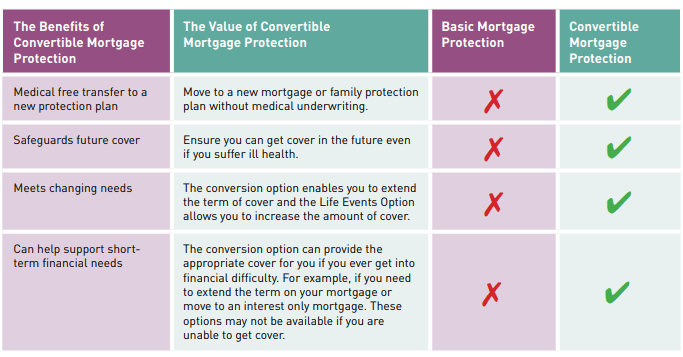

When I first wrote this blog, way back, there was no conversion option available on reducing life insurance policies so you couldn’t extend them. Since then Zurich Life, Royal London, Irish Life and New Ireland have all added a conversion option to their reducing life insurance policies.

The conversion option is magic. It allows you to convert/turn your reducing life insurance into level term life insurance at any time in the future without answering medical questions. Think of it as a safety net in case you change your mind and decide you would prefer level term life insurance.

I know this is a little bit complication so if I have melted your head, I am sorry…?…but if you complete this life insurance questionnaire, I can do the thinking for you and send you a personalised recommendation ?

BTW if you’re online looking for a reducing life insurance quote, you can get one here but remember to change the dropdown option to mortgage protection!

Finally, if you’d like a quick chat to discuss, please schedule a time here.

Talk soon

Nick

As Ireland's leading life insurance broker, we specialise in comparing the rates and policies from the top five Irish life insurance providers and offering the very best value quotes to suit the individual needs of our clients. Our expertise lies in finding a suitable insurance plan for those with specific needs, be it a particular illness, occupation or claim history, we've got you covered in every sense!

Watch our video