Are you ready for some truth?

You’re screwed if you can’t work.

And if you have a family who depends on your income, well they’re fecked too.

Imagine trying to pay the mortgage, all the bills and live on illness benefit of €232 per week.

Impossible.

That’s why protecting your income is the most grown-up thing you can do especially if

I’m sure you’ve heard about serious illness cover and you may have even heard whispers about income protection but you need to know more.

So you’ve come to the right place.

Here’s a breakdown of the key differences between Income Protection (also known as Permanent Health Insurance) and Serious Illness Cover (also known as Critical Illness Cover and Specified Illness Cover).

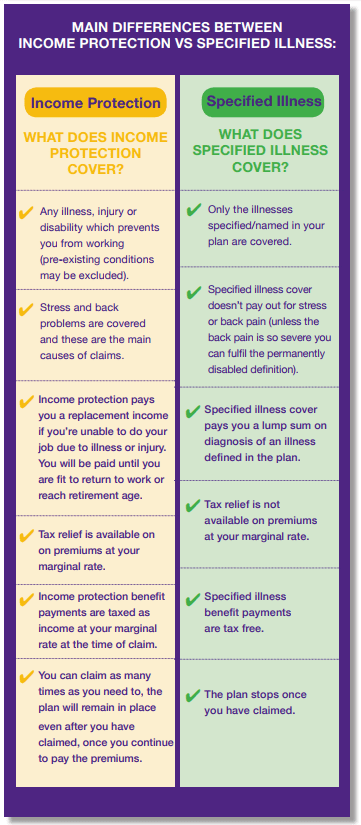

Here are the main differences between income protection and serious illness cover in handy chart form!

Let’s look at those differences in more detail.

Salary protection will payout for ANY illness, injury or disability that stops your doing YOUR job (pre-existing conditions may be excluded)

But serious illness cover will only payout if you get one of the illnesses listed on your policy.

Income continuance will pay out if you can’t do your job for longer than the deferred period due to a mental health issue or if you can’t do your job because you hurt your back/pulled a hammy/cricked your neck/stubbed your toe (badly). In fact, these issues make up a huge percentage of income protection claims.

However, a serious illness policy won’t payout for mental health or musculoskeletal (nice word Nick) issues.

Serious illness cover pays you a one time, tax-free, lump sum on diagnosis of an illness defined in your policy.

Whereas income insurance pays you a regular, recurring, taxable income if you’re unable to do your job due to any illness.

You can claim tax relief on income protection at your marginal rate. This means you can get up to 40% back on your premiums.

There’s no tax relief on serious illness cover.

But you’re taxed on income protection payouts

What the taxman giveth with one hand he taketh away with the other.

Although you get tax relief on your premiums, you pay income tax, PRSI, USC on the payout

Serious illness payouts are tax-free.

Looking at it another way, you get guaranteed tax relief on income continuance even if you never make a claim.

You can claim as many times as you need to on your income protection. Your plan will continue even after you have claimed, once you keep up the premiums.

Your serious illness policy will end once you have made a full claim.

Any illness, injury or disability severe enough to prevent you from doing your job (pre-existing conditions are excluded) for longer than the deferred period.

As I mentioned, but it’s worth reiterating – stress and back problems are covered and these are major causes of claims.

You can read more about what income protection covers you for here.

Only the illnesses specified/named in your policy are covered.

So serious illness cover doesn’t pay out for stress or back pain (unless the back issue is so restrictive that you’re classed as permanently disabled)

4,8,13,26 or 52 weeks – depending on the deferred/waiting period you choose.

You’ll receive a single tax-free lump sum.

One word of warning, if you have serious illness cover on a policy that’s assigned to the bank for a mortgage, the bank will receive any payout!

Whaaaaaaaat?

Read more here – Don’t add serious illness cover to your mortgage cover.

When buying car insurance, do you choose Third Party, Fire & Theft or Fully Comprehensive?

Critical Illness is like Third Party, Fire & Theft.

It pays out for pre-defined, specific events only like types of cancer, heart attack and stroke.

Income Protection is like Fully Comp.

Income Protection covers anything that incapacitates you or stops you working like stress or back pain (neither of which are covered by serious illness cover)

Most of us prefer the security that fully comprehensive car insurance offers.

I’d say the same for income protection.

H/T to Matthew Chapman for the analogy.

PAYE Worker on €100,0000

You can insure up to 75% of your income less state illness benefit of €10,556 per annum.

Let’s say you earn €100,000

If you’re an employee, you can cover a maximum income of €64,444 per year (75% x €100,000 – €10,556).

If you make a claim, the insurer will pay €64,444 and you can claim €10,556 from the state = €75,000 in total.

Self Employed on €100,000

If you’re a sole trader or a company director, you can insure the full €75,000 because you don’t get illness benefit from the state.

You get nothing if you can’t work.

Your income drops to a big, fat ZERO.

Get a quote for 75% cover – if you’re self-employed, you. my friends are a loon if you don’t have income protection.

You choose the amount of insurance you need

e.g if you buy €75,000 serious illness cover, you’ll get a tax-free lump sum of €75,000 should you contract a specified illness listed on your policy.

I’ve considered income protection but feel that any absences of more than a couple of months are likely to be due to a serious illness, at which point serious illness cover would kick in?

I see where you’re coming from but I’m afraid serious illness cover isn’t that comprehensive.

The main reasons people cannot work long term are mental health and musculoskeletal disorders (limbs, back and neck pain).

Remember, serious illness cover won’t pay out if you’re out of work due to stress or joint pain.

With serious illness cover, there’s a danger that the illness that prevents you from working either

For example, you’d assume if you got cancer, your serious illness cover would pay out immediately?

Afraid not, cancer has to be of a specified severity in order to get a full payout.

What you don’t want is to be out of work and hoping your illness gets so severe that you get a payout.

That’s an awful situation to contemplate.

Income protection, on the other hand, pays out if you cannot do your job due to ANY illness, injury or disability.

If your budget can stretch to it, by all means, put some serious illness cover in place too…maybe one year’s after-tax income.

That payout will give you the flexibility to take 12 months off work unpaid if you suffer a critical illness so you can focus on getting better without money worries.

But to safeguard your income long term, you can’t beat income protection.

By the way, did you know the average duration of an income protection claim is 5 years?

You’d need to buy a geansai-load of serious illness cover to cover 5 years income.

Mental maths: multiply your income x 5, it’s a big number isn’t it?

You don’t have to choose either income protection or serious illness cover.

It might be a case where buying a little of both is the best way to protect yourself.

Serious illness cover covers immediate, short term expenses.

Income protection replaces your income long-term and allows you to get on with your life. That’s why it’s called Long Term Disability Cover in other countries.

Income protection and serious illness cover are complex products, please take advice from a professional (or me, if they’re all busy)

Want to learn more about income protection – have a nose through our free guides.

Or read this whopper:

Here’s a good run-through of income protection and serious illness cover from The Sunday Times that we helped with:

If you’re weighing up income protection and serious illness cover but are a bit stuck, let me help…that’s what I’m here for.

Complete this questionnaire and I’ll take a look at your personal situation and make a recommendation for you.

Or if you prefer to have a quick chat first, excellent, I’m all ears.

I look forward to hearing from you

Chat soon.

Nick

As Ireland's leading life insurance broker, we specialise in comparing the rates and policies from the top five Irish life insurance providers and offering the very best value quotes to suit the individual needs of our clients. Our expertise lies in finding a suitable insurance plan for those with specific needs, be it a particular illness, occupation or claim history, we've got you covered in every sense!

Watch our video