Inheritance Tax (Capital Acquisitions Tax or CAT) can’t usually be avoided altogether, but with proper planning you can significantly reduce its impact. Understanding the tax-free thresholds, making use of available exemptions and, where appropriate, arranging a Section 72 Life Insurance policy can help ensure your children inherit more of your estate instead of Revenue.

Fill out this short form and I’ll work out the most affordable way to protect your kids from Revenue. No waffle. No pressure. Just straight-up advice.

You may believe inheritance tax is a rich person’s tax that won’t affect you.

But if you intend to leave a property worth over €400,000, it will affect you.

And this doesn’t take into account any other assets your children may receive on your death – cash, investments, cars.

So if a €400k house makes you rich, welcome to the Country Club (the hostesses will be round with canapes soon).

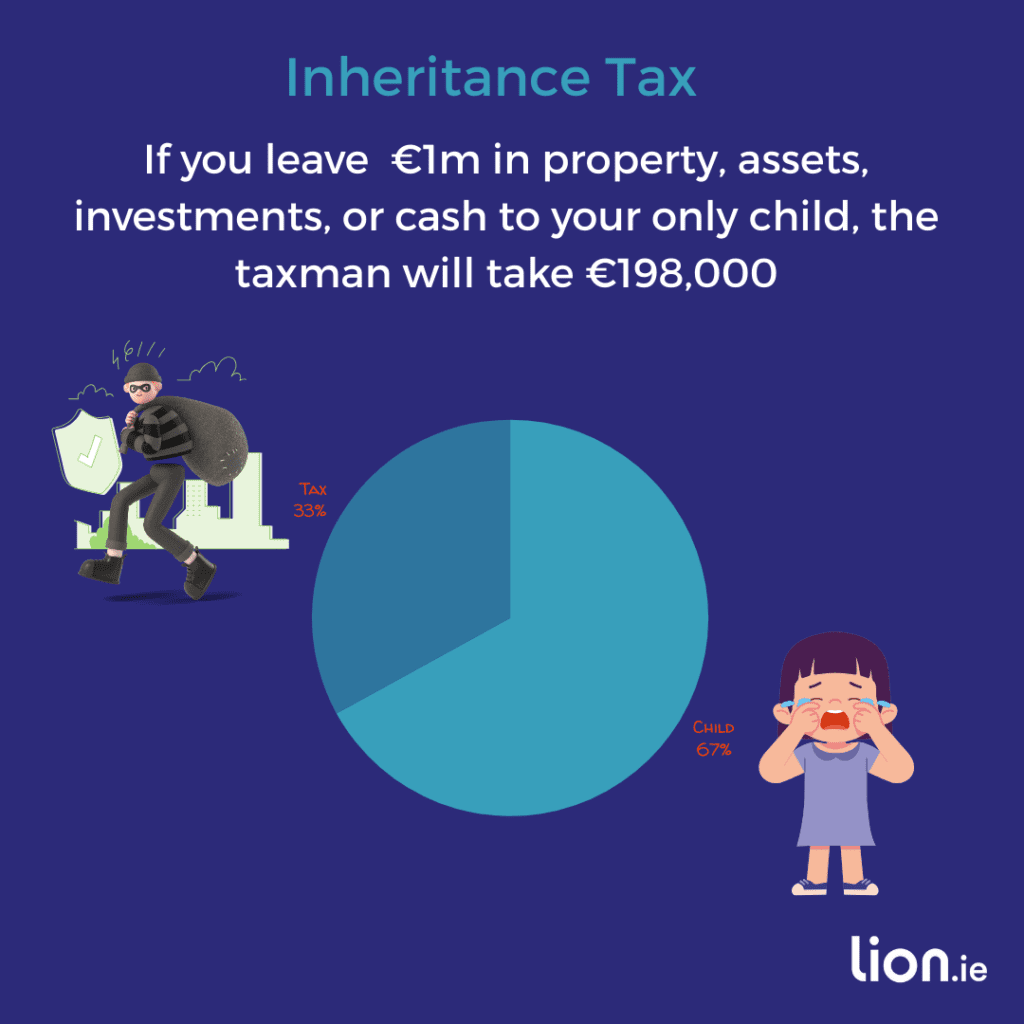

But let’s go mad and say your total assets are worth a cool million.

Here’s what his or her nibs will have to stump up in tax before they can get his hands on any of it.

Whether you think inheritance tax is fair or unfair, the reality is that many Irish families will have to deal with it.

What I can do is show you how to plan ahead, so the Taxman doesn’t help himself to a chunk of your kids’ inheritance.

Let’s start with the basics…

CAT isn’t something most of us deal with every day, so don’t worry if you’re not entirely sure what it is.

It’s essentially a tax on receiving something of value — and it comes in two forms:

This article is all about helping you prepare for the second one — inheritance tax — because, well… death and taxes, as the fella says.

If you’re a spouse or civil partner, good news — you won’t pay inheritance tax on anything you inherit from your other half.

Everyone else?

They’re on the hook.

And it’s usually your children who are most at risk.

The more they inherit, the bigger the potential tax bill.

If the value of what you inherit is under your tax-free threshold (we’ll cover that in a sec), you’re in the clear.

But anything over your threshold?

It gets hit with a hefty 33% tax.

Let’s break it down from your children’s point of view:

Say your two children are inheriting €1.5 million worth of assets from you— that includes property, savings, jewellery, cars, crypto, the lot.

Assuming they’ve received no previous gifts from you, they are each looking at an inheritance tax bill of €115,500

And here’s the kicker — Revenue wants that in cash.

Miss the deadline?

Revenue will happily slap on penalties and interest until it’s paid.

They might be able to arrange a deferral, but eventually, they’ll still have to cough up €115,500 each

Sure, I could walk you through all the steps and formulas…

But honestly, who has the time (or the desire) to make their brain melt trying to figure it all out?

Much easier: use a calculator.

Here’s the one I recommend from Zurich→

Not sure how much inheritance tax your children could face? Use Zurich’s free calculator to get an estimate in under two minutes.

The result is an estimate only. Future asset values, tax thresholds and Revenue rules may change over time.

Let’s go back to the example above.

They are inheriting €1.5 million from you

But this time, let’s say they have already received €100,000 each from you in the past — maybe from a gift or earlier inheritance.

That €100,000 eats into their Group A threshold, reducing it from €400,000 to €300,000.

Now their taxable inheritance jumps to €450,000 (€750,000 – €300,000), leaving them with an inheritance tax bill of €148,500

Once their threshold is fully used up, every cent they inherit from you gets hit with a 33% tax.

No discounts.

No mercy.

If the parents are married or in a civil partnership, they can pass assets between each other completely tax-free.

So inheritance tax doesn’t usually bite after the first parent dies — the surviving spouse simply inherits everything without a bill from Revenue.

The issue comes later:

That’s when inheritance tax kicks in — and often, it’s a big number.

To avoid leaving your children with a surprise tax bill (and a scramble to find the cash), parents should consider taking out a Section 72 Life Insurance Policy.

This special type of cover pays out on the death of the second parent, and — here’s the magic bit — the payout is Revenue-approved to cover the inheritance tax bill so it isn’t liable to tax.

More on how Section 72 works in a bit…

Yep — and they can make a big difference to your final tax bill.

There are a few special reliefs that can reduce the amount of inheritance tax owed, depending on your situation. Here are the main ones:

Explaining all the rules for these would melt your brain (and break this blog), but if you think any of them might apply to you, you should contact someone with a bigger brain (specialist tax advisor).

📌 We can help with the next step.

One of the most effective ways of planning for inheritance tax is a Revenue-approved Section 72 life insurance policy.

Rather than reducing the tax bill itself, it provides your beneficiaries with the money to pay it, helping them avoid selling assets to raise the cash.

Read our complete guide to Section 72 Life Insurance →

That’s a pretty comprehensive look at preparing for an inheritance tax bill.

In my experience, there are two types of people in the world:

If that’s you, fair play and best of luck — but we’re probably not the right fit (and that’s grand too).

If that sounds like you, we’d be happy to help you understand your family’s likely inheritance tax exposure and whether a Section 72 policy makes sense.

📅 Schedule a call:

📧 Email: [email protected]

Written by Nick McGowan, QFA RPA APA

Nick is a qualified financial advisor and founder of Lion.ie, a multi-agency Irish life insurance and income protection brokerage based in Tullamore. He’s been helping people secure fair, transparent cover for over 15 years and was named Protection Broker of the Year 2022.

If you’d like straight answers without the sales pitch, learn more about Nick here.

057 93 20836

Ask a question

As Ireland's leading life insurance broker, we specialise in comparing the rates and policies from the top five Irish life insurance providers and offering the very best value quotes to suit the individual needs of our clients. Our expertise lies in finding a suitable insurance plan for those with specific needs, be it a particular illness, occupation or claim history, we've got you covered in every sense!

Watch our video