I take it you’re here because you’re looking for advice on income protection?

You’ve figured out that you need to plan ahead just in case bad shit happens.

And because the alternatives to income protection insurance just don’t cut the mustard

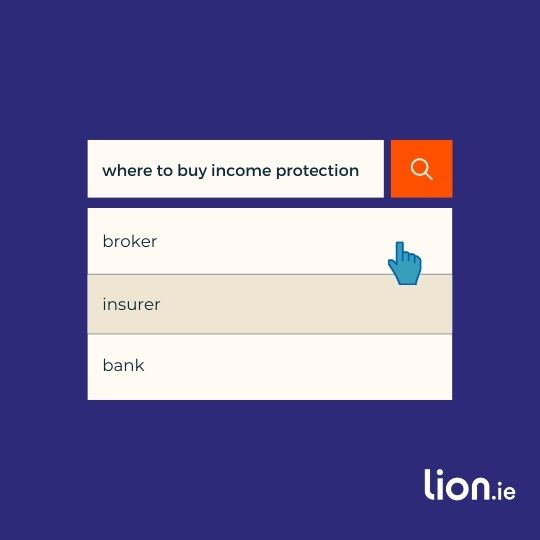

But where you should buy it?

I can see you’re far too clever, you know they can only sell their own policy (usually from Irish Life)

Yeah right, again, you know they can only sell their own policy.

Ah, now we’re getting somewhere. A choice of 5 insurers.

But which broker?

Let me outline the case for lion.ie 🙂

Yes, I know that seems like I’m setting the bar very low.

But there are some who just sell sell SELL.

That’s not my style – but don’t take my word for it.

So what do we do instead?

We offer advice on policies from

We answer your questions.

We outline which company will suit you best.

Then we get out of your way and give you some time to breathe and take it in.

Buying income protection is an important decision and one that’s not to be taken lightly.

If you decide you want to go ahead with us as your income protection broker, happy days!

If not, hopefully, you’ll be impressed enough with our service to tell your friends.

We know our onions when it comes to income protection.

You see, we’re a specialist protection broker (mortgage protection, life insurance, serious illness cover and income protection).

We don’t claim to be protection experts while also trying to flog you a pension, gadget insurance and something to cover Rover and Fluffy.

This gives us the time to focus 100% on knowing income protection inside and out.

We know income protection is a bit of a minefield and we’ll guide you through it without getting you blown up.

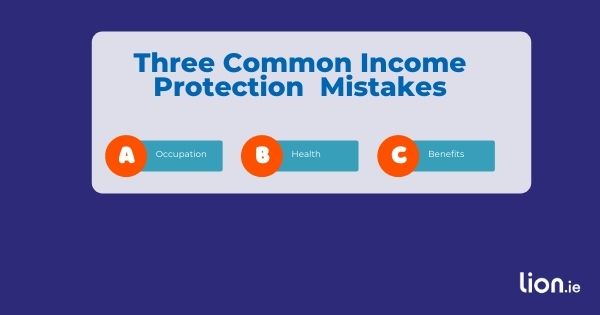

Insurers classify your occupation according to the risk of having to pay a claim.

So people who work in higher-risk jobs pay a higher premium

e.g an electrician will pay more than an accountant for the same amount of cover because on average, their risk of injury is higher.

That seems fair enough, yes?

Risk 1 = lowest risk, Risk 4 = highest risk

But did you know some insurers give a different risk rating to the same occupation!

Recently I arranged cover for a retail manager (he was a manager in Aldi).

Avvia, New Ireland, Royal London and Irish Life classed him as a Risk 2 (remember, the higher the risk class, the higher the premium).

But Aviva classed him as a Risk 1 saving him a small fortune over the life of his policy.

I’m not saying Aviva are always the most lenient when it comes to occupations though…

During the summer, I arranged cover for a marine engineer:

Royal London classed her as a risk 2, Irish Life and New Ireland classed her as a risk 3 while Aviva classed her as a risk 4.

Last week, I got a plumber covered, one insurer classed him a risk 3, the other classed him as a risk 4.

As you can see, you need to be very careful here, don’t accept a higher risk rating from one insurer without checking out the others.

Work with an income protection broker who knows their way around.

Income protection pays out if you are unable to do your job due to any illness, injury or disability…excluding pre-existing conditions.

Pre-existing conditions include any previous health issue

e.g

You see income protection in underwritten much more strictly than life insurance or critical illness cover.

A sprained wrist isn’t going to result in a death or serious illness claim but for someone who works on a keyboard, it could lead to an income protection claim.

But some insurers are more “trigger happy” than others and will add exclusions like a chef adds salt.

Other insures are fairer.

Again, don’t accept an exclusion, question it and check with the other insurers to see if the can offer cover without that exclusion.

Choose an income protection broker who knows which insurer is best for your particular health issue.

If we haven’t come across your condition before, we’ll speak to all 5 insurers to get you the best deal out there.

All income protection policies are not the same.

This article is too short to go into all the differences in detail (go here instead) so here’s a snapshot (click to enlarge)

As you can see, no insurers offer identical benefits.

So if an income protection broker tells you all the policies are the same, “just pick the cheapest”, you know what to do.

Leg it!

If you like the sound of what we do, greater, we’d love to help.

Please complete this questionnaire and I’ll be right back with a no-obligation recommendation and an indication of cost.

Thanks for reading

Nick

As Ireland's leading life insurance broker, we specialise in comparing the rates and policies from the top five Irish life insurance providers and offering the very best value quotes to suit the individual needs of our clients. Our expertise lies in finding a suitable insurance plan for those with specific needs, be it a particular illness, occupation or claim history, we've got you covered in every sense!

Watch our video