If you’re looking for income protection for your job, you’re in the right place.

Start by finding your role below. Then we’ll show you how insurers are likely to assess it and where people get caught out.

Quick heads up: we recently saw a Civil Engineer given Class 1 (lower) rates by two insurers but Class 2 by three others. Same job, different premium.

Not sure how your job will be viewed?

Tell us what you actually do (not just your job title) and we’ll tell you how insurers are likely to assess it.

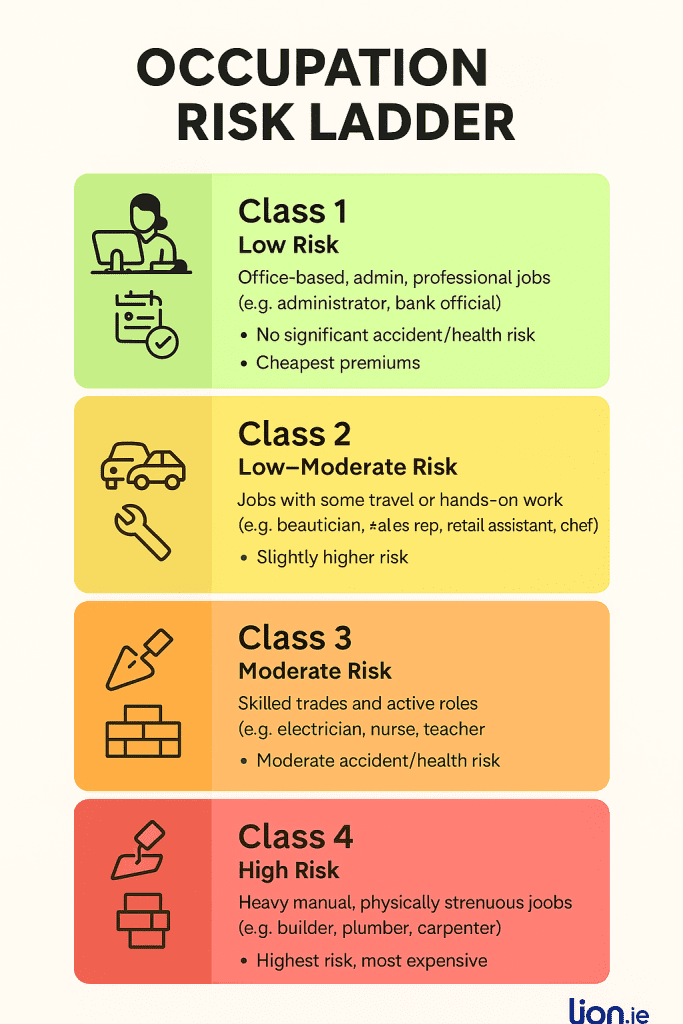

Insurers don’t just look at your age and health, they also look at what you do for a living.

Every job is placed into an “occupation class”, which reflects how risky that job is from an insurer’s point of view.

Lower-risk jobs (like office-based roles) usually get better terms.

More physical or hazardous roles can mean higher premiums or a decline (not all occupaitons can get income protection)

We recently looked at a case for a civil engineer working with Irish Rail.

On paper, it looked straightforward. Mostly office-based, occasional site visits, and supervisory work.

But when we checked with insurers:

That’s a completely different outcome for the exact same job.

The difference came down to how each insurer interpreted the site work:

If this client had applied to the wrong insurer first, they could have ended up with higher premiums for no reason.

Most people get this wrong the first time.

If you apply to the wrong insurer first, you don’t just get a worse quote but you can limit your options going forward.

We check all five insurers before you apply so you don’t have to guess.

Editor’s note: First published August 2025. Updated in 2026 to reflect how insurers in Ireland currently assess different occupations for income protection.

Written by Nick McGowan, QFA RPA APA

Nick is a qualified financial advisor and founder of Lion.ie, a multi-agency Irish life insurance and income protection brokerage based in Tullamore.

He’s been helping people secure fair, transparent cover for over 15 years and was named Protection Broker of the Year 2022.

If you’d like straight answers without the sales pitch, learn more about Nick here.

As Ireland's leading life insurance broker, we specialise in comparing the rates and policies from the top five Irish life insurance providers and offering the very best value quotes to suit the individual needs of our clients. Our expertise lies in finding a suitable insurance plan for those with specific needs, be it a particular illness, occupation or claim history, we've got you covered in every sense!

Watch our video