When you think about buying your first home, you probably think of the good stuff.

You’re not going to be thinking about the crap stuff like

But does anything ruin romantic notions quite like considering what’d happen if one of you died?

It’s not exactly the pillow talk that solid relationships are built on.

We’ll start with the first step: get your mortgage approval.

Given the current state (in ‘the bleedin’ hack of it’ sense) of the housing market in much of Ireland, you’ll probably be buying with de other half.

It may be a matter of convenience.

It may not ?

You’ll have saved your deposit by living in your parent’s house for the last year and giving up every single fun thing you love.

Once you’ve done all that, you’ll need mortgage protection to seal the deal before your lender will part with the dosh you need to buy your home.

Mortgage Protection Insurance clears your debt to the bank if you die.

So, if you (or your partner) meet an early, very sad end, your home becomes theirs, debt-free.

If you didn’t have Mortgage Protection, the debt would keep on keepin’ on and there’d only be one of you to pay it off – which, again, given the apocalyptic state of the housing market, would be really, really rough.

Anyway, the lender won’t actually give you a mortgage without Mortgage Protection, so you’re gonna have to cough up for it, whether you want to or not.

But!

That doesn’t mean you should buy Mortgage Protection Insurance from your bank/lender.

In fact, you probably shouldn’t.

This leads nicely to question numero uno in this unofficial FAQ.

Don’t buy from your bank for two reasons:

Bank prices are much more expensive because they are stuck with one insurer.

PTSB, AIB, KBC and Ulster Bank can only sell Irish Life insurance.

Bank of Ireland are limited to Bank of Ireland insurance.

Let’s look at an example to see how much more you’ll pay:

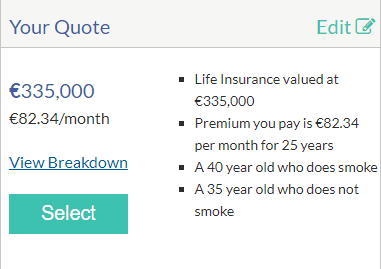

You’re a 40-year-old smoker and your partner is a 35-year-old non-smoker. Don’t worry, soon you’ll be a non-smoker due to the constant nagging and tutting.

Your mortgage is for €335,000 over 25 years.

You’re both in good health but your partner is convinced that cancer is only around the corner because of the smokes.

I tried to get a quote on the PTSB website but it transferred me straight to the Irish Life portal.

They are quoting €82.34 per month.

We can offer the same level of mortgage protection for €53.37

That’s a saving of €8,691 over the life of your policy.

Imagine the damage you could do in IKEA

Buying from the bank may seem handy – sure you’re in there already!

But think of it like this: what happens if you find a better mortgage rate somewhere else?

If you buy a BLOCK policy with a bank, they will cancel your policy if you switch to a new lender.

Think about it, if you find a better mortgage deal, you’ll have to reapply for cover. You’ll be older and possibly ‘iller’ – which could seriously hit you in the pocket, and sure mortgages are pricey enough as it is.

Worse, if you have had a serious health scare, you might not be able to get mortgage protection so you’ll be stuck paying too much for your mortgage.

If you go with a broker, they can compare all available policies on your behalf and you can take your policy with you if you switch.

Making the wrong choice really could end up costing you thousands, so think long and hard before you sign up for Mortgage Protection with your lender.

With a Joint policy, there is one pay-out on the first death.

So let’s say you have a heart attack and shuffle off this mortal coil.

The bank gets the pay-out, i.e. your mortgage is cleared and your other half gets to keep your home mortgage-free.

With a Dual policy, there are two pay-outs.

Yes: two.

So let’s say you die first because you didn’t quit smoking.

The mortgage is cleared.

Your other half soon passes away from a broken heart, such is their love for you, then your family/dependents/cats get a second payout.

Dual Mortgage Protection Insurance used to be much more expensive, but that’s not the case anymore.

So it just makes sense to go with Dual.

Your feline family will be dining on the finest tuna the world can produce for the rest of their luxurious nine lives.

In short: yes.

If insurance had commandments, number two would be ‘thou shalt always take a conversion option’. (Number one being: ‘thou shalt get insurance with Nick @ Lion.ie). ?

Hand on heart, you’d be bananas not to get a Convertible Mortgage Protection Policy because it lets you:

All without having to answer a single health question.

So even if you’re on death’s door, the insurer has to extend your policy.

There’s not much else to say about it, so moving swiftly on!

A chronic illness shouldn’t affect your chances of getting Mortgage Protection.

Emphasis on: shouldn’t.

In some rare cases, the insurer might think the chances of you having to make a claim are too high so they might postpone or decline you.

Every application is assessed by underwriters who’ll consider the likelihood of a claim (in hard terms: that you die during your cover).

If you’re seriously ill, you could see why the underwriters (and the insurer, by extension) would baulk at covering you, but I promise this rarely happens.

If you have a minor health issue, you’ll have to complete a medical questionnaire.

If you have a serious illness, the insurer will request a report from your GP.

GPs can be a bit interminably slow, so don’t leave this too late as I’ve seen insurer’s requests for reports being eaten by fax machines (remember fax machines?) for weeks or even months, and you don’t want that ruining your chance of buying a house.

If you have an underlying condition, the key is getting prepared early and hitting up the insurer who’ll be the most sympathetic to your case.

Each of the five insurers assesses illnesses differently, so get in touch with a sound unbiased broker (who me? Ahwouldyastop!) so they can match you up with the insurer who’s best for your particular health history.

You can thank me when you’re giving your other half the cold shoulder after an unmerciful row in IKEA over cushion covers.

Interested in Mortgage Protection Insurance?

Complete this short questionnaire and I’ll send you some quotes asap, it’ll be quicker and easier than doing it yourself.

If you have a couple of questions you’d like me to answer first, call me on 05793 20836 for a quick chinwag.

Thanks for reading

Nick

lion.ie | Protection Broker of the Year ?

As Ireland's leading life insurance broker, we specialise in comparing the rates and policies from the top five Irish life insurance providers and offering the very best value quotes to suit the individual needs of our clients. Our expertise lies in finding a suitable insurance plan for those with specific needs, be it a particular illness, occupation or claim history, we've got you covered in every sense!

Watch our video