Table of Contents

You can do it all online: fill in a magic quote machine and buy it there and then.

Done.

However, it’s not quite simple if you’ve got health issues or a dangerous job.

You’ll have to pay more for your cover because the insurers think you’re high risk (more chance you will make a claim).

It’s not fair, but that’s why we’re here—to ensure you pay as little extra as possible.

However, even if you’re fit as a proverbial fiddle, you could end up spending way too much if you choose the wrong insurer.

Let’s look at an example.

Sarah is 40 years old and in good health.

She wants a cool million in cover because she’s just welcomed her second baby (it’s amazing how having a second baby focuses the mind)

The baby looks like a little old man, but Sarah thinks he’s cute, and that’s the important thing here.

Sarah goes to her bank for advice.

The bank recommends Irish Life because most banks are tied to Irish Life, and they give Sarah a quote that’s tenner more expensive, per month, than a similar policy available through a broker.

That tenner, across 25 years, adds up to €2,979.

Wave goodbye to that €2,979, Sarah

It gets worse if you have a significant health issue because the insurers will “load ” their base premium.

A loading is a nice way of saying “add an extra wedge to your premium”.

It’s already hard enough dealing with a chronic illness only for the insurers to go and take a metaphorical, money-fuelled dump all over you, but that’s what happens.

But you can beat them at their own game.

You see, loadings differ from insurer to insurer because each insurer takes a different view on how “serious” an illness is.

For example, let’s say Sarah has well-controlled Type 1 Diabetes.

Depending on the insurer she chooses, the loading will vary from an extra 125 percent per month to an extra 225 percent.

An example will clear things up.

Let’s say Zurich decides to hit Sarah with a loading of 125 per cent, and the bank’s insurer hits her with a loading of 225%

If Sarah trusts the bank and takes that policy, she will pay €15,402 EXTRA OVER THE LIFE OF HER POLICY

Which is an abomination!

The important thing is to find the best insurer for YOUR situation.

No two people have identical health issues, so no two insurance policies will be underwritten identically.

So, now you know the cold, hard numbers, what can you do to ensure you get the best deal?

It’s hard to know where to start with different insurance companies, plan types, and benefits.

So, let’s start at the very beginning.

Remember, you’re not meant to know anything about life insurance at this stage.

But there are a few basic life insurance concepts you need to master to protect your family.

By the way, we have a life insurance crash course that simplifies this into 5 bite-sized emails. If you don’t have time to read this whole article, you can sign up here:

You’ve got three options.

A bank can only sell you a policy from their tied insurer.

A bank cannot offer life insurance advice on a range of policies from various insurers.

Again, this limits your options.

If you go to Zurich, they will sell you a Zurich policy.

Approach Aviva and they can only sell you an Aviva policy.

A decent life insurance broker can offer policies from the five leading providers in Ireland.

If you feel your broker is slinging policies from just one insurer, beware!

Some “brokers” are also tied to one insurer – yeah, I know, this a bit sch-neaky so be cute.

The beauty of a “real” broker is choice, advice and discounts!

This is the tricky part.

You can try to figure it out yourself using any of the 987 life insurance calculators you can find online (I’ve counted them)

You can also get guidance from a bank, insurer, or broker (with the caveats above).

But please, if any of them recommend €250,000 over 25 years, make your excuses and leave.

€250,000 is the same as plucking a figure out of thin air.

You could do that yourself.

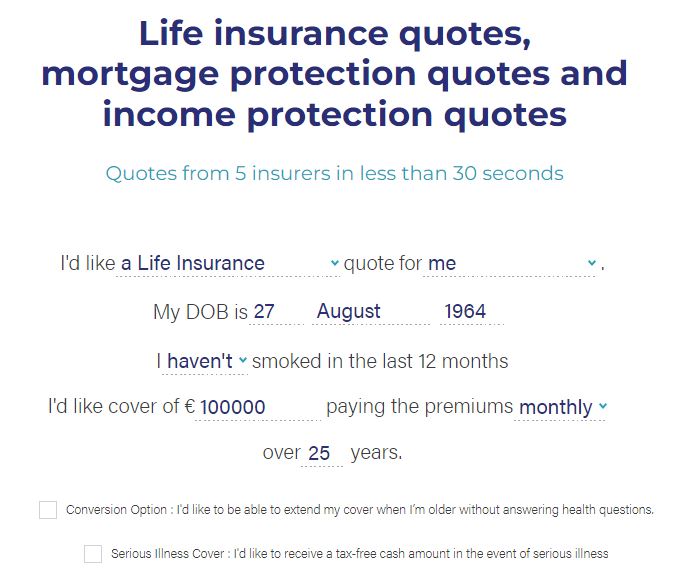

Our instant calculator will give you a more helpful recommendation.

How do you figure out the correct amount of life insurance?

Death, inability to work, and serious illness are the risks that will hit us or our families right in the pocket.

Each type of life insurance policy offers protection from these risks.

Here’s a quick breakdown of the policies available

Yeah, not that type of quote.

This type:

Most banks, insurers and brokers have an online quote system.

The beauty of ours is we don’t force you to give us your contact details.

We know how annoying follow-up sales calls are, so we don’t do them – unless you ask us to!

We give you time and space to make a decision.

If you choose, we will arrange your cover.

Yey!

If not, hey-ho, can’t win ’em all; we’re just happy we played some part in getting you and your family covered.

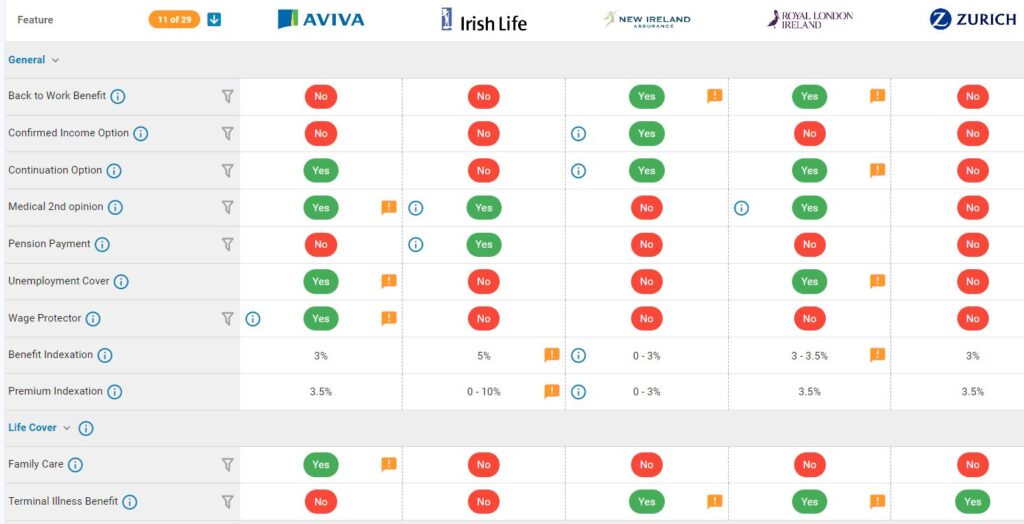

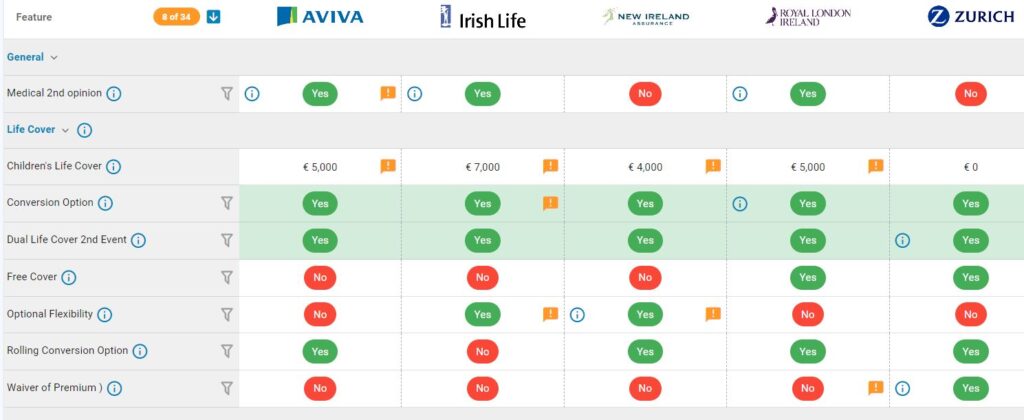

Which insurer should you choose?

Your options are bewildering, but I can help.

Here are some handy charts that compare what’s on offer at each insurer

There are too many illnesses to list, but Royal London and Zurich Life are the best for covering serious illnesses.

Still with me?

If you have no health issues, this is the simpleton’s guide to choosing an insurer 😋

When promotional discounts are available, we immediately reduce our online quotes so you know you’re getting a competitive price.

Aviva, Zurich, New Ireland and Royal London offer discounts.

Irish Life doesn’t offer any discounts – why would they? They are creaming all that business from the banks 😆

We discount the prices on our quote system, no shenanigans here, what you see is what you get.

We don’t make you haggle to get the best price.

Who needs that?

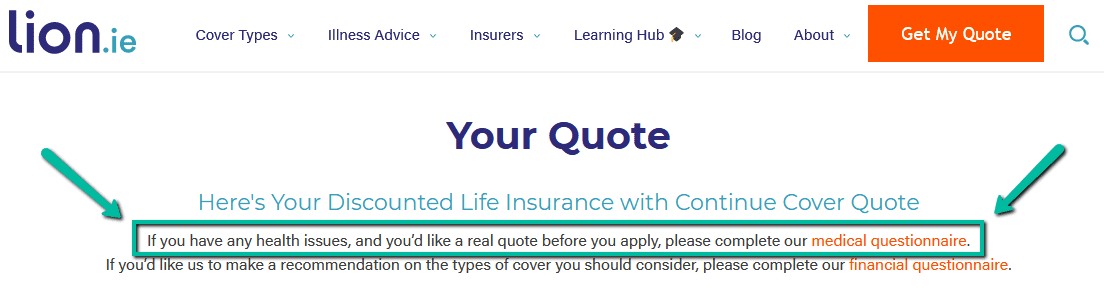

The initial quotes you get, whether from a broker, bank, or direct from the insurer, assume you’re in perfect health.

So, if you have any current or previous health conditions, you may pay more than that initial quote.

Therefore, it’s important to run any health by your advisor before you make an application so they can find the most suitable insurer for your condition.

As you can see on our quote system, we highlight this fact:

We don’t give you some unrealistic quote to get you to apply and then hit you with a ludicrously more expensive quote after you answer the medical questions.

What’s the point?

You probably won’t be interested in the cover at the higher premium, so we’ve wasted your time and ours.

If you have health issues and want an accurate quote, please tell us about them upfront.

You can read more about the life insurance medical conditions we specialise in here.

I hope that gives you the basics of choosing a life insurance plan.

If it all makes sense and you’re confident you can do it yourself…fire ahead.

But if the thought of arranging your cover without getting advice makes you do this…

We’re here for you!

Complete this questionnaire, and I’ll be right back.

![]()

Thanks for reading.

Nick

Editor’s Note : We first published this blog in 2017 and have regularly updated it since

As Ireland's leading life insurance broker, we specialise in comparing the rates and policies from the top five Irish life insurance providers and offering the very best value quotes to suit the individual needs of our clients. Our expertise lies in finding a suitable insurance plan for those with specific needs, be it a particular illness, occupation or claim history, we've got you covered in every sense!

Watch our video